For “Scripture Sunday”:

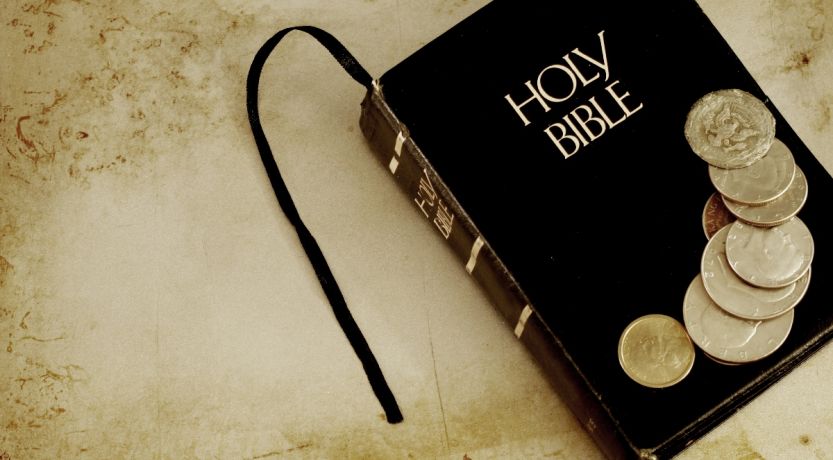

Slave to the Lender

“Credit is an easy way to buy what you want now. Used wisely, credit can be an effective tool; but without restraint, it can make you a slave to the lender.

Don't become a slave to the lender.

The importance and usefulness of credit in our modern life is evident. The value of a good credit rating is emphasized by the prevalence of credit reporting and credit protection products and companies. A poor credit rating can be a rude awakening for someone trying to buy a house—or even applying for a job!

A culture of credit

For the average family, a major purchase such as a new automobile or a home would not be possible without the ability to borrow money on credit and pay it back over time. Many businesses must also occasionally borrow money to upgrade facilities or purchase equipment. Without sufficient capital on hand, credit becomes an important means to keeping a business growing and profitable.

These are important uses of credit in our society today. And used wisely, it allows a family or a company to take advantage of opportunities that would otherwise be lost. Gains in business and equity for a family are all positive outcomes of credit used wisely.

Not all credit is created equal

Continued at: https://lifehopeandtruth.com/relationships/finances/slave-to-the-lender/

_________

Six Biblical Personal Finance Principles

“Money affects every aspect of our lives, and God’s financial principles can help us gain control and find peace of mind.

The other day it seemed that just about every conversation I was part of or overheard related to money.

At lunch, a friend told me she needed to take a second job to pay for her son’s college tuition. Another friend called me, discouraged about her upside-down car loan. A radio talk show host discussed consumer debt levels with his listeners. The couple behind me in line at the supermarket argued about whether they could afford certain items in their shopping cart. After receiving our latest utility bill, my husband and I had a long chat about how we could cut back on energy usage.

Truthfully, that day probably wasn’t much of an aberration—for me or for the people I was in contact with. The fact is, our personal finances influence much of what we think about, talk about and do day in and day out.

Often we’re worrying about whether we’ll have enough money to make ends meet, pay for an unexpected expense or retire. Some people become obsessed about amassing their fortunes and turn into workaholics. I’ve known people whose mood changed, depending on what the stock market was doing or how many bills were outstanding.

Our finances affect where we live, our work schedules, what we do with our free time and on and on.

So it’s not surprising that the Bible—the owner’s manual for living—has a great deal to say about money.

What follows are six biblical personal finance principles, along with some elaboration from professional financial consultants.

1. Follow a budget

The Bible doesn’t use the term budgeting, yet it offers clear direction on the importance of such planning. Simply put, a budget is a written plan to track and control income and expenses.

Proverbs 27:23 says, “Be diligent to know the state of your flocks, and attend to your herds.” Put in modern terms, we need to be aware of how we’re using our income, so we can know whether we need to make adjustments in our spending.

“Budgeting helps us avoid impulsive and unnecessary spending, live within our means, and prepare for future needs,” explains Bill Gustafson, senior director of the Center for Financial Responsibility at Texas Tech University. “If we don’t carefully plan our finances and direct them where to go, we will one day find ourselves broke.”

To set up your household budget, figure out how much you spend each month for different categories (such as housing, food, transportation, entertainment, clothing, medical, etc.), and compare that to your monthly income. If your expenses are more than your income, you will need to cut out unnecessary purchases.

Once you’ve established your budget, use either a ledger or a budgeting program on the computer to start tracking your monthly expenses. “If you get to the point where there’s no more money left for the month in a particular category, stop spending,” Dr. Gustafson says. “It’s going to take some determination to do this, but it’s a necessary step if you’re going to get your finances under control.”

For more on budgeting, see our online article “The Bible, Budgeting and You.” It includes a downloadable sample outline budget.

2. Tithe faithfully

The top priority on our income, before we do anything else with it, should be God’s tithes. God says in Malachi 3:10, “Bring all the tithes into the storehouse, that there may be food in My house.”

A tithe is 10 percent of a person’s “increase” (Deuteronomy 14:22), which is given to support the ministry and work of the Church. When we tithe, we show God that we are putting Him first in our lives.

Certainly God doesn’t need our money. Everything we have ultimately belongs to Him (Exodus 19:5). The real beneficiaries of tithing are those of us writing the checks. In the last part of Malachi 3:10 God makes the promise that when we faithfully tithe, He will “open … the windows of heaven, and pour out … such blessing that there will not be room enough to receive it.”

The blessings can be physical or spiritual. Financial expert Dave Ramsey explains in his blog that tithing teaches us to be good stewards of what God has given us and to live unselfishly. This can lead to improved household finances and can help us become better spouses, friends, relatives, employees and employers.

Tithing can also help us learn to trust God more fully and build a closer relationship with Him. Often people who tithe can think back on times when—at least on paper—it didn’t look like they could afford to tithe. Yet they did and had enough—sometimes even more than enough—for their physical needs.

One friend put it this way: “Tithing has helped me to stay more focused on God, to not just look at the ‘facts’ from a human perspective, and to remember we can always count on God in all situations.”

3. Avoid unnecessary borrowing

The Bible warns against the use of debt. Proverbs 22:7 states, “The rich rules over the poor, and the borrower is servant to the lender.” If you become burdened with a heavy load of debt, in essence you’ve become a slave to your creditors. You no longer have the freedom to decide how to spend your paycheck because you’re obligated to meet those debts.

The way to keep debt in check is to be careful about buying on credit. “Only borrow for purchases that will increase or hold their value, such as home or college tuition,” advises Erica Sandberg, a San Francisco–based money management consultant. “Don’t take out high-interest loans for nonessential items that are likely to depreciate quickly, such as new automobiles, clothing, furniture, appliances or jewelry.”

According to a 2018 report from Creditcards.com, the average credit card interest rate in the United States is around 17 percent. This means you’ll pay $170 in interest annually on every $1,000 of debt.

According to a 2018 report from Creditcards.com, the average credit card interest rate in the United States is around 17 percent. This means you’ll pay $170 in interest annually on every $1,000 of debt. If you let the balance carry over month after month, you can quickly end up owing far more than the original price of your purchases.

Erica Sandberg recommends only using credit cards if you are able to pay the full balance on the statement each month, so you don’t have to pay any interest. If you have a lot of outstanding revolving debt, this should be paid off as quickly as possible, starting with the credit card that has the highest interest rate.

4. Save up before spending

Financial planners generally suggest saving at least 10 percent of your income every month. Have three different accounts: a short-term savings for major purchases (such as new household furnishings or vehicle repairs), a long-term savings (for your retirement or children’s college tuition), and an emergency fund (in case of a job layoff or large unexpected expense).

“Saving up money before making a purchase is one of the smartest ways to keep out of financial trouble,” says Dr. Gustafson. “By having money set aside for ‘big ticket’ items, you won’t be tempted to use credit cards to pay for them.”

This is another biblically based financial principle. Proverbs 21:20 says, “Be sensible and store up precious treasures—don’t waste them like a fool” (Contemporary English Version). Proverbs 6:6-8 describes the ant, who saves during a time of plenty for a time when there will be need. We, too, should save now for future expenses.

5. Give to others

Everything we have—our money, physical assets, jobs and even the ability to earn money—comes from God (Ecclesiastes 5:18-19). After meeting our own needs, He wants us to share some of what we’ve been given with others.

In Acts 20:35 Paul quotes Jesus as saying, “It is more blessed to give than to receive.” We should give unconditionally—even when the recipients cannot repay us (Luke 14:12-14). That could mean donating to charity, buying someone a gift, having people over to dinner or buying food for a homeless person.

While we need to exercise wisdom in how much to give, we shouldn’t be so tight with our money that we’re reluctant to part with any of it. As with tithing, God blesses us when we’re generous (Luke 6:38; 2 Corinthians 9:6).

There have been times when I’ve given and afterward seen a disconcerting emptiness in my pocketbook. But then seemingly out of nowhere I received some unexpected cash or other financial blessing that filled that gap.

When we have the desire to share, God gives us the means to do so.

Of course, not everyone has the same financial means. We may genuinely be struggling monetarily. But even then, we can still give of the time, talents or other nonfinancial assets that God has provided for us. The point is, God wants us to use what He has blessed us with so we can be a blessing to others, not just so we can fulfill our own needs and desires.

6. Put your confidence in God, not in your finances

When it comes to finances, people often go from one extreme to another. If our bank accounts, retirement portfolios and home values are increasing, we might start trusting in them. When we’re facing a job layoff, stock market losses or unplanned expenses, we may worry anxiously. Neither extreme is the biblical approach.

The Bible makes it clear that true security can only be found in God (1 Timothy 6:17) and that trusting in riches will destroy us (Proverbs 11:28). Our wealth and possessions are temporary and can easily be wiped out in an instant, perhaps through theft, accidents or natural disasters.

If we’re struggling with our finances, we must remember that God is our refuge, and that He cares for those who trust in Him (Nahum 1:7). We shouldn’t be anxious about money problems (Philippians 4:6). We must do our part—to not overspend, but to save and invest our money in what has eternal value. The rest is in God’s hands. If we’re seeking God’s Kingdom first and foremost, we can be assured that God will provide for our physical needs (Matthew 6:25-34).

By committing to these financial principles, we will benefit from improved finances and financial peace of mind. There may be less tension about money at home and a better connection among family members as well.

Most important, we will learn to trust God more fully, develop a deeper appreciation for His purpose for us and build a closer relationship with Him.” From: https://lifehopeandtruth.com/relationships/finances/six-biblical-personal-finance-principles/?

---------

Update.

One reason that I chose these topics is because when I left England it was the rule that you had to put a third down on something you wanted to get on credit, “on tick”, they called it. I think that stopped a lot of unecessary debt, which is too prevalent these days. So I hope that folks will go by these good principles when borrowing.

Just regular maintenance around here this week. Raking and burning and trying to keep abreast of the leaves and pine needles, and we also had to burn some old termite-eaten lumber. One morning I took Zack to the local food pantry operated by the local churches, to get his ration of free food.

On Wednesday, I took a day off and looked in various thrift shops. in Conroe. One find was “The Bible from 26 Translations” and I also bought one of those old glass electric hot plates, but this one is about 3 feet long. It will keep a lot of the church potluck food at serving temperature. My daughter called my cell while I was at Walmart ordering my new eye glasses, she was in Conroe so we met and I saw her new German Shepherd pup, “Ruckus” for the first time. He is big. I tried to take a picture, but he wouldn’t hold still.

On Thursday, the usual Yoga and Senior exercises at the “Y” and they put on a lunch there this time. Friday, a visit to the doctor, just routine stuff, and then because it was “Preparation Day”, according to the Bible, I got my church clothes ready, cooked for the church potluck, and set my hair. A quick brush through and it might look decent.

For the Sabbath potluck I took Turkey Spaghetti Bolognese, Whole Grain crackers and White Cheese dip. I also took the rest of that enormous cookie that had been taking up room in my deep freeze. But the favourite dessert there was a cheescake, and that went fast!

The Bible readings were Gen. 49:1-27, Zech. 14:1-11, Luke 23:13-34 and all of Matt. 7. The teaching was the second part of “Messiah, Our Advocate”.

The computer guy was at church this time and now I have my desktop back, hurray! Even though I found out how to use my regular monitor instead of hunching over the table-height laptop screen, it just didn’t do right for me. It has Windows 8 and I am used to Windows 7. I hope I never have to get used to Windows 10! The keyboard is a little different, too, so that made me make mistakes,

Still crazy weather around here, you can’t get bored. Really cold, and then just to surprise us, a warm day.

No comments:

Post a Comment